If you’ve spent any time on econ Twitter or econ Bluesky since 2022, you’ve almost certainly come across the idea of the “vibecession.” For the uninitiated, the vibecession essentially says that starting in 2022, the “vibes” about the economy became significantly negative and out of line with the fundamentals of the economy which were, and continue to be, fairly strong. Opinions about the vibecession, and whether it’s even a thing, are varied. I’ll get into the different camps shortly. In this post I wanted to explore an idea: perhaps, to the extent that the vibecession exists, anxiety over AI job losses could be playing a role. In the next section I’ll break down the vibecession debate further. After that I’ll present my idea and then I’ll get into the evaluation of my idea. Unfortunately, the data does not seem to bear out my theories. But in the interest of doing my part in the war against publication bias, I wanted to write it up anyway

The Vibecession

Arguments about the vibecession break down into a few camps. One camp, led by prolific Poster Will Stancil, argues that the gap between the sentiment and actual economic performance is due to misleading and false viral content on social media and the increasingly Balkanized nature of news consumption. Another camp, whose chief proponent may be G Elliot Morris, argues that the gap can be explained by the price level, that is, people are upset not about inflation (i.e., the year-over-year increase in prices) but instead that things are more expensive than they were in 2021. I’d definitely recommend reading his post on the topic. The final camp argues that, actually, the economy IS bad and the fundamentals (inflation rate, unemployment rate, etc) do not capture the full picture. They point to rising credit card debt and surveys claiming that a high percentage of Americans can’t afford basic necessities.

Another major player in the Vibecession Wars I would be remiss to not include is the economist Matt Darling. He seems to fall into the first camp but spends most of his time arguing with people in the third camp. I would also suggest reading his post on the subject, as it is the inspiration for my post.

A fan of nuance, I think each side has its merits. The extent to which the fundamentals and sentiment diverged (more on that in a minute) certainly seems strange and sudden. However, I don’t think that misleading viral Bluesky posts are the whole explanation. I’m pretty sympathetic to Elliot Morris’s theory, but I also tend to think that there are deeper issues in the economy that aren’t captured in the headline numbers. For instance, it seems like a bad sign that auto loan defaults are at their highest recorded rate.

Modeling Consumer Sentiment

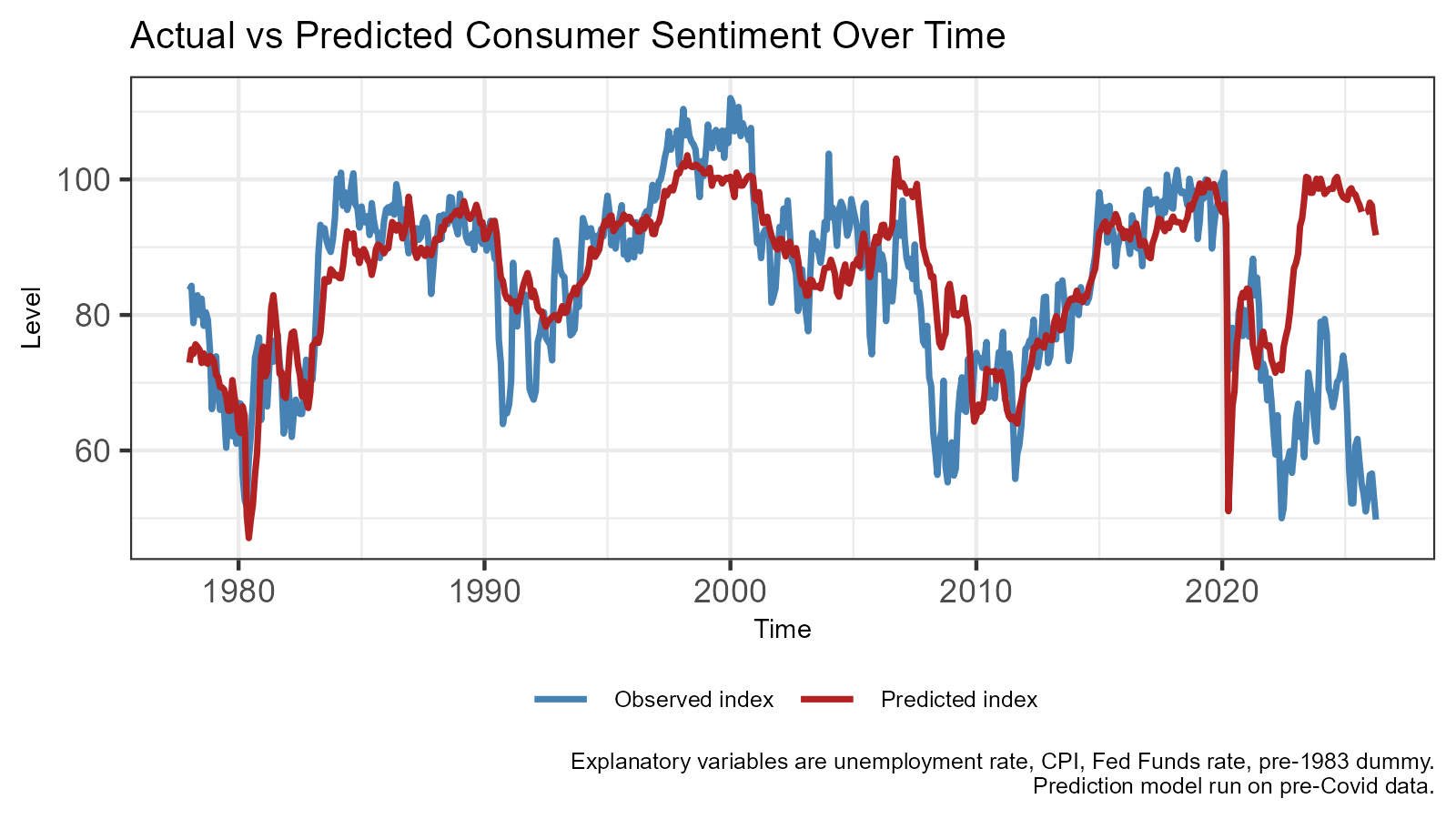

The main data source that people use when identifying the vibes in the vibecession is the University of Michigan Survey of Consumers Index of Consumer Sentiment. Below I have graphed the index the along with a predicted version of the index using the unemployment rate, inflation rate, and Federal Funds interest rate from the per-Covid time period. The methodology is shamelessly stolen from Matt Darling, who has basically the identical graph in the post linked above.

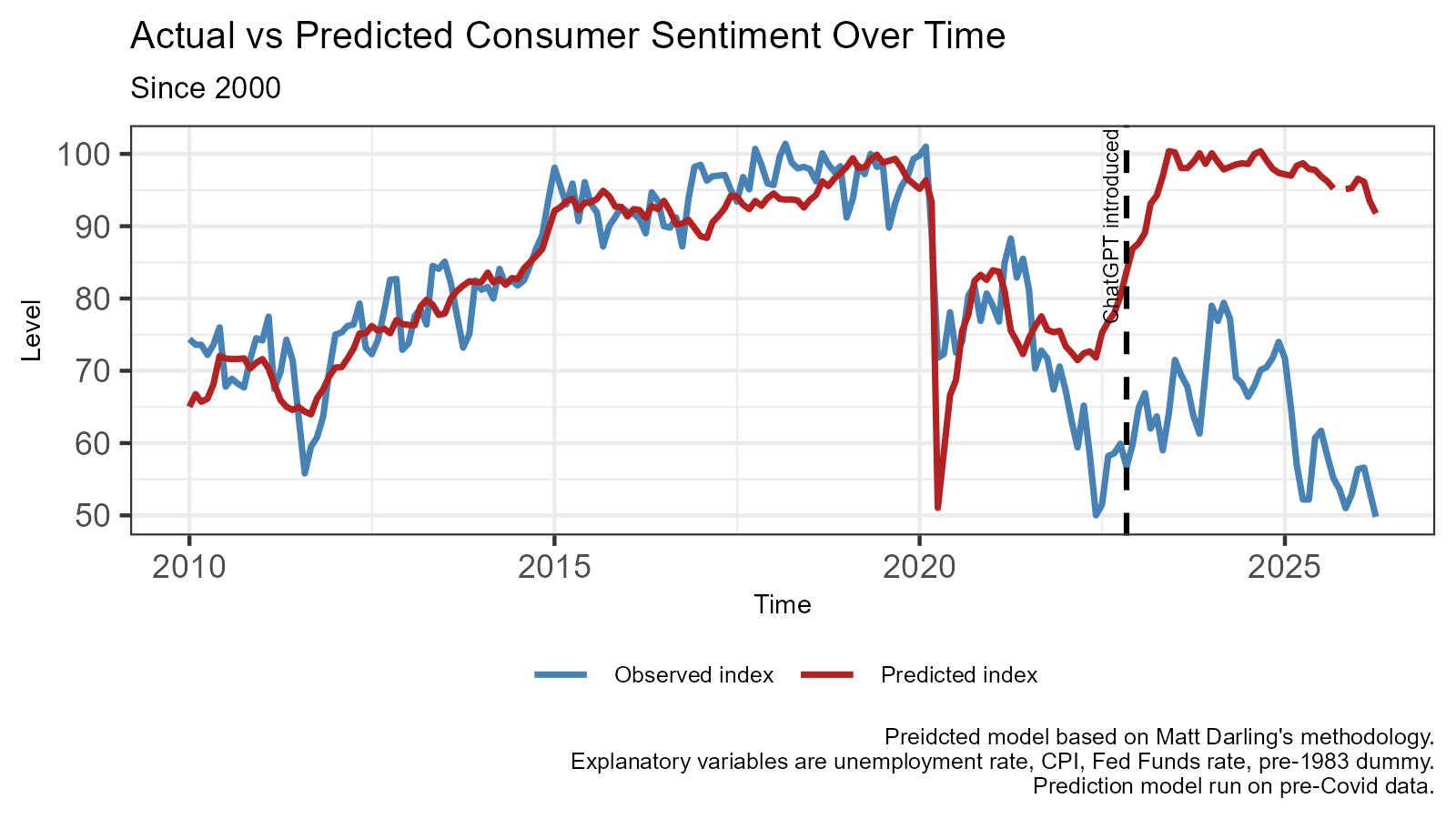

You can see that predicted sentiment roughly matched predicted sentiment up until a clear divergence in 2022 when sentiment became increasingly negative while the fundamentals of the economy stayed relatively strong. When I saw this graph on Matt’s Bluesky, it struck me that 2022 was also when ChatGPT was released, and I wondered if the constant barrage of stories about how everyone is going to lose their job because of AI may have caused people to feel more negatively about the economy than they “should.” Below, I added the introduction of ChatGPT to the data to the graph and zoomed in a bit.

Now, the timing doesn’t line up exactly, as the divergence began before ChatGPT was released, but I still figured AI job anxiety could play a role in sentiment remaining low for four years.

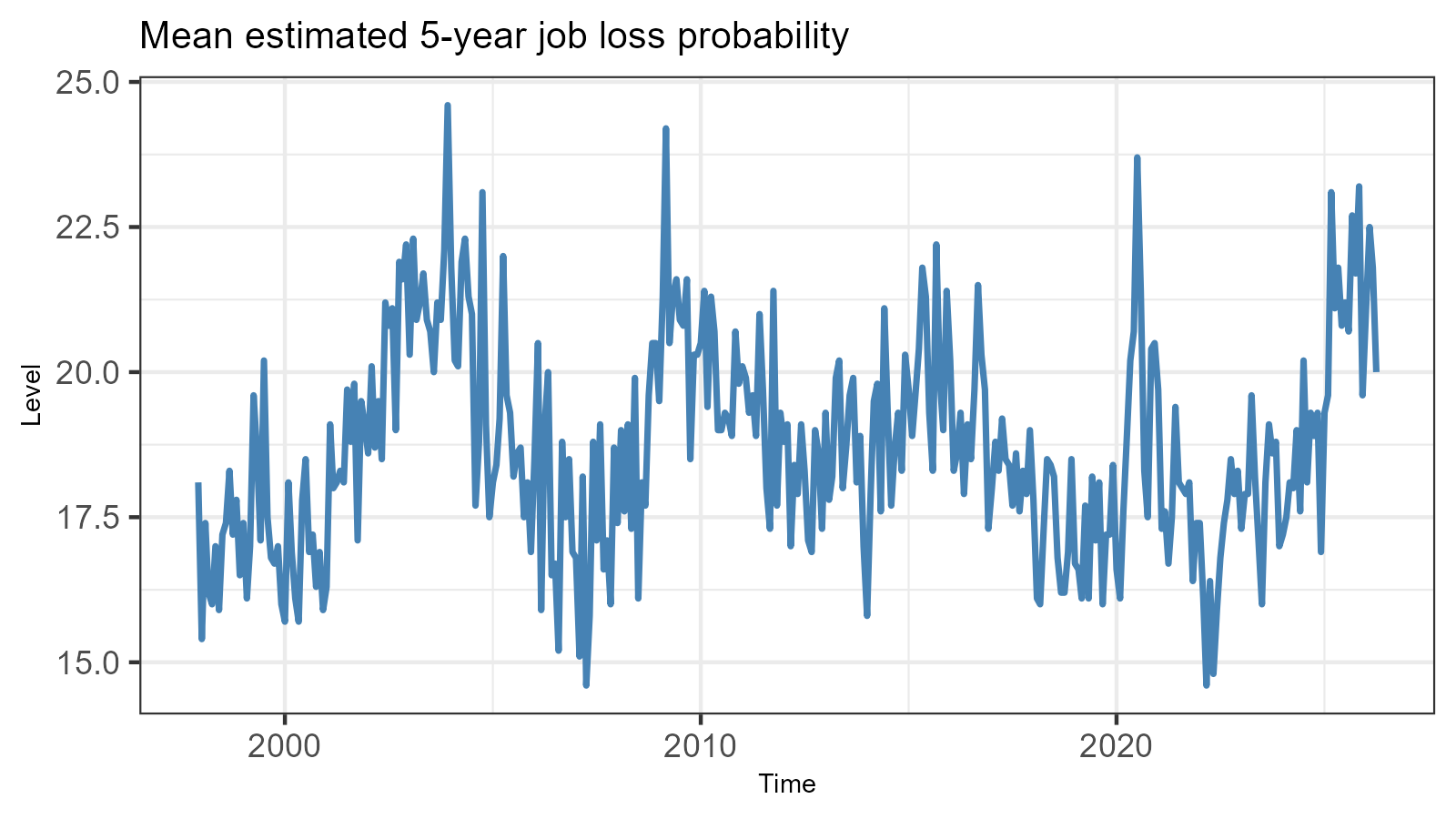

To that point, the Michigan Survey of Consumers offers evidence that job anxiety is high, even though unemployment is low. In addition to the overall sentiment index, the survey also asks respondents additional questions about their feelings about the economy. One of these asks each respondent to estimate the probability that they will lose their job in the next five years. In 2025, the mean probability reached a remarkably high level for how low the unemployment rate is. My theory is that this is due to AI, and that this helps cause the bad economic vibes.

Grok, Did AI Cause the Vibecession?

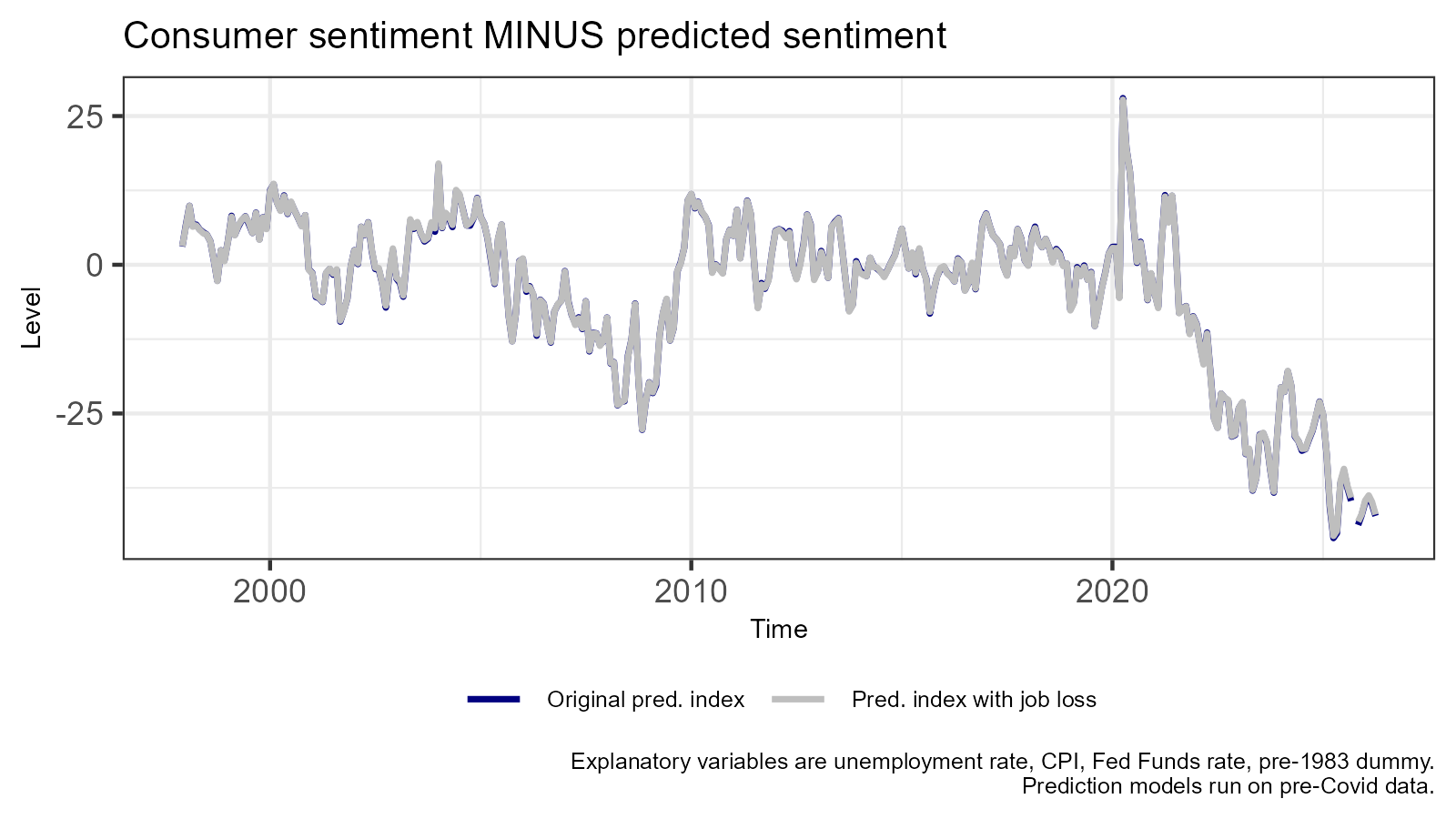

And now, I get to test my theory. Following Elliot Morris’s approach in his post, I reran my predicted consumer sentiment model, but with the mean five year-job loss estimated probability included as an explanatory variable. (Because the survey only began asking the job loss question in 1997, I ran both the original prediction model and new model on the data since 1997). The idea here is that if anxiety about job loss is causing people to have more negative feelings about the economy overall, the model that includes this variable should track closer to consumer sentiment than the original model.

For ease of comparison, instead of showing the consumer index and the predicted values, this graph shows the index minus the predicted values for the two models.

As you can see, the two models overlap almost perfectly, meaning that adding the job loss variable makes virtually no difference. It hardly moves the needle in terms of improving the predictive power of the model. I was a little disappointed in this result, but it is possible that AI job anxiety could still be playing some role in the vibecession; perhaps this variable is just not a good way to capture that anxiety. I had hoped to bring a peaceful resolution to the Vibecession Wars, but sadly, that was not to be. In any case, thank you for reading!

0 Comments